%20-%20Transparent%20bkg%20.png)

This is the second article in our series covering the value of Roth IRAs. To read the first article, click here.

Contributing to a traditional IRA or a tax-deferred employer plan like a 401(k) may seem like a winning strategy on the surface. You get the combined benefits of an immediate tax deduction from your contribution and you avoid paying taxes on any growth in the account each year. However, this “winning strategy” has an expiration date.

When a Good Deal Turns Sour

Once you begin taking money out of your tax-deferred accounts in retirement, the good deal that you were receiving goes away and that income gets taxed at ordinary income tax rates.

In addition to paying ordinary income tax rates on all contributions and growth in the account, the greater risk is that the government can change the rules at any time and increase your tax bill when you pull money out of your tax-deferred savings account.

How Things Change

Regardless of your opinion about upcoming tax changes, one thing is certain: the tax cuts that American taxpayers received in 2017 will be expiring in 2025. This means that taxes are increasing for most Americans, even if the Biden administration fails to pass their proposed tax plans.

For example, a married couple in the 24% tax bracket today is likely to see their marginal tax bracket increase to the 28% or 33% tax bracket when the tax cuts expire in January of 2026.

A recent example of how Congress can change the rules is the SECURE Act. As discussed last week in our intro discussion to Roth IRAs, Inherited IRAs are now required to be withdrawn over a 10-year period. With the likelihood that your heirs will still be working when you pass, these forced withdrawals may push them into higher tax brackets.

Your Options

Given the current tax laws, there are essentially two main choices for addressing the challenges we just laid out:

You can continue maxing out your IRA or 401(k) each year and deferring taxes for as long as possible. And then you can hope that tax rates don’t increase (while the US government continues to run up spending and debt).

You can shift your contributions to the Roth bucket and begin converting some of your tax-deferred savings to the Roth IRA now, while tax rates are still low. In doing this, you are essentially “buying out” the government’s fractional ownership of your IRA.

To do the latter, you will have to do something that we are hard-wired to avoid: pay more taxes now. Although this approach seems to violate logic, option number two may create a much-lower lifetime tax liability.

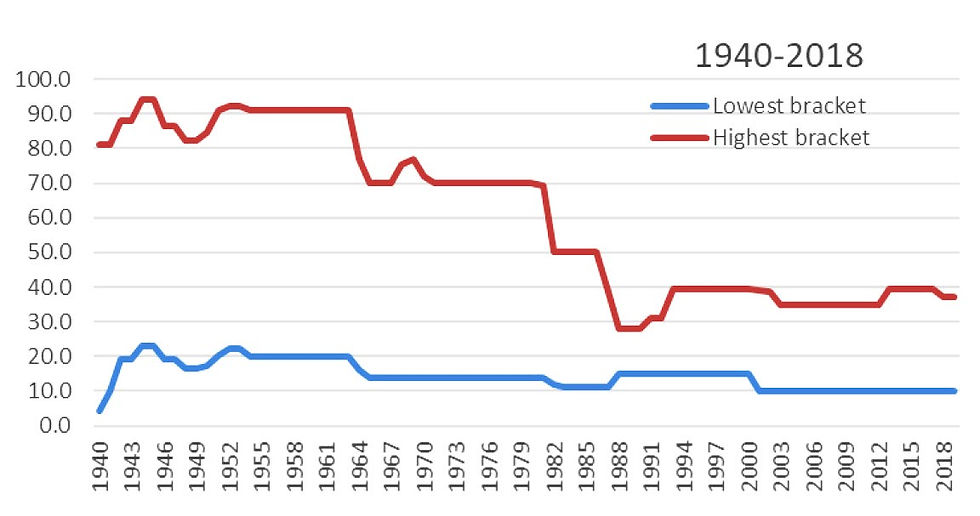

When reviewing historical tax rates here in the US, we can observe that we are currently in a period of extraordinarily low tax rates. Combining our historically low tax rates with a rising national debt, the probability of tax rates rising in the future is high.

The logic behind option number two is that the current tax rates allow taxpayers to convert tax-deferred IRA savings into Roth IRA savings at rates that may not be seen again for decades. The combination of new IRA rules and the impending 2026 tax increase means the historical approach of building a large tax-deferred IRA or 401(k) may result in more revenue for the IRS and less post-tax money for your retirement.

Other Considerations

Aside from your capacity to pay tax and save today, there are other things to consider when converting to a Roth:

How large is your pool of retirement assets?

What are your other sources of income in retirement?

What percent of your savings is in the tax-deferred, taxable and never-to-be-taxed-again buckets?

What is your projected tax bracket for the next few years?

What is your projected tax bracket in retirement?

What is the projected tax bracket of your beneficiaries when you are in your 80’s?

What state do you/your beneficiaries live in and what state do you plan to live in retirement?

With questions like these in mind, making the annual decision to convert IRA or 401(k) money into a Roth IRA can be tricky. And that’s where Monotelo can come alongside you to help you make fully-informed decisions that perfectly align with your most-deeply held values and long-term goals.

This article is a general communication being provided for informational and educational purposes only and is not meant to be taken as tax advice, investment advice or a recommendation for any specific investment product or strategy. The information contained herein does not take your financial situation, investment objective or risk tolerance into consideration. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel. Any examples are hypothetical and for illustration purposes only. All investments involve risk and can lose value, the market value and income from investments may fluctuate in amounts greater than the market. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions, inflation or US tax policy. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

Comments